What Is Economic Resilience?

The under-theorized concept at the heart of American industrial policy

This is a cross post between ChinaTalk and Factory Settings. Founded by Jordan Schneider, ChinaTalk is a hybrid think tank and media outlet with deep expertise on China and emerging technology. Factory Settings is a publication led by the former CHIPS Program Office senior leadership about state capacity and industrial policy. Interested readers can subscribe to ChinaTalk here and Factory Settings here.

In recent years, a range of objectives has been offered to justify industrial policy, from tackling climate change to boosting growth to asserting geopolitical dominance. But no objective has proven more durable, more bipartisan, or more influential for policy than the catch-all of “resilience.”

Resilience is rightly a core objective of industrial strategy and served as the central motivation for the CHIPS and Science Act, which aimed to reduce dependence on Taiwan for the supply of semiconductors.1 But for all the consensus on resilience as a core objective, it is not clear how to translate that general aim into a sound national industrial strategy.

At CHIPS, we learned this the hard way as we sought answers to questions that would define our investment strategy: How much of our portfolio should we allocate to leading-edge production as opposed to other critical technologies? How much of that production should we try to onshore? What should we do about other chokepoints in the leading-edge logic supply chain, like advanced packaging or EUV lithography? How could we use creative award terms to fortify our industrial base?

These are the types of specific questions that emerge when crafting industrial policy for a single industry. But they are downstream of more foundational questions that any policymaker seeking to build resilience through industrial policy will need to ask as they determine which industries to target and how.2 This piece is an attempt to set forth and answer what we see as three threshold questions that should inform any resilience-based strategy:

What is resilience, and what do we need it for? In response to what contingencies might a resilience-based industrial strategy be warranted?

What are the sources of resilience? What should a resilience-based industrial strategy seek to build, and how will we know if it has succeeded?

How much resilience is enough? How do we know when a resilience-based strategy is worth it?

What is resilience, and what do we need it for?

We understand resilience as the ability to withstand external shocks, and resilience-based industrial policy as aimed at withstanding external shocks by ensuring access to goods that are critical for national security or the broader economy. In a narrow sense, resilience is an economic concept: how vulnerable the economy is to shocks from abroad. But it is also a political one, corresponding to our ability to sustain political objectives under external pressure.

There are three types of shocks that resilience-focused policies may seek to address. These shocks may result in increases in demand (category 1) and disruptions to supply (categories 2 and 3):

The first category is public emergencies that rapidly increase demand. The quintessential example is a large-scale military conflict. In the event of such conflict, a country must be able to sustain the pace and intensity of military operations in a range of realistic scenarios (e.g., a six-month conflict vs. a two-year conflict; a one-front war vs. a war on multiple fronts). Resilience requires anticipating such scenarios and ensuring sufficient supply of military equipment — for example, missiles, drones, interceptors, and artillery shells — across various possible outcomes. As detailed in a prior piece, America’s most extraordinary industrial policy success in this category was the buildup of defense manufacturing in World War II. At its peak, American industry supplied roughly two-thirds of all Allied military equipment produced during the war, including some 193,000 artillery pieces.

Another example of a public emergency is a pandemic, which similarly requires countries to procure in advance or quickly produce the materials and equipment necessary to respond, such as PPE, test kits, and vaccines. This category does not include the broader and less predictable potential economic ramifications of a pandemic — factories idling due to sick employees, supply chain disruptions — which are included in the third category below.

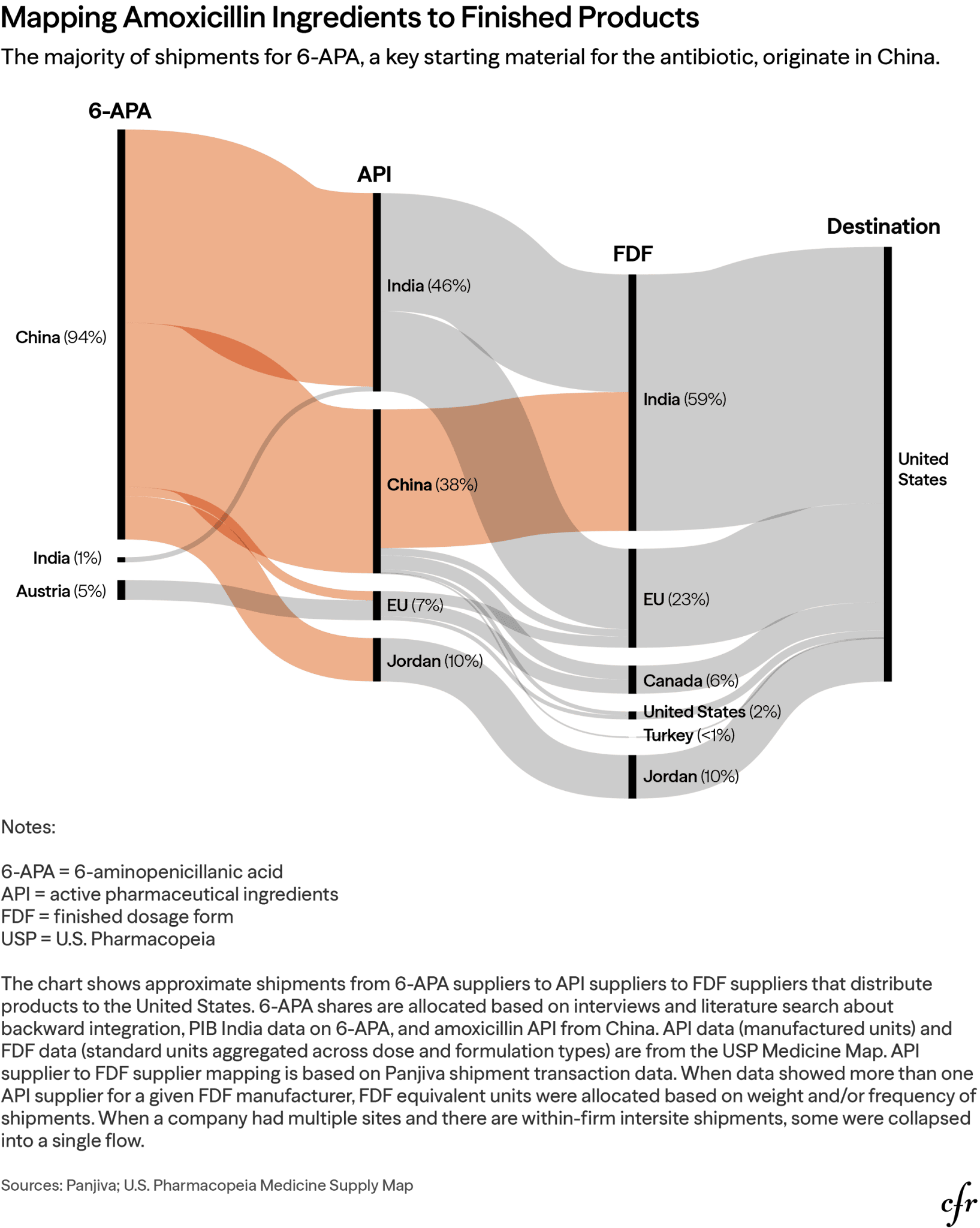

The second category is geopolitical coercion, which is when an adversary weaponizes critical supply chains to extract political concessions or otherwise advance political aims. A prototypical example is China’s April 2025 decision to cut off access to rare earths, which would have resulted in the idling of factories across America; rather than accept that consequence, the Trump administration shifted its political posture, offering to relax tariffs and semiconductor export controls. Given the scale of China’s industrial investments, the threat it poses extends well beyond rare earths. China also controls key portions of several other critical supply chains that it has not yet leveraged but could in the future — active pharmaceutical ingredients, for example, where it controls the raw or starting materials for 94% of amoxicillin, 74% of heparin, and 70% of acetaminophen. Resilience to geopolitical coercion means being able to withstand a disruption for long enough that an adversary fails to secure its political objectives.

The threat of geopolitical coercion exists during both peacetime and war. In a military conflict, an adversary will be more likely to activate all sources of leverage it might deploy in peacetime, and then some. What’s more, in wartime, chokepoint vulnerabilities are not limited to supply chains that an adversary currently controls: it can exploit additional chokepoints through military strikes, cyberattacks, and naval blockades that sever access to other sources of supply. In a military contingency over Taiwan, for example, one can imagine China taking a range of such measures to exploit US semiconductor dependency to advance its political objectives. Building resilience to geopolitical coercion therefore requires taking into account not just the leverage a potential adversary currently holds, but also the broader range of vulnerabilities it could activate or create.

The final category is a broader group of random shocks and collateral damage to global supply. Unlike the first category, this category describes shocks to supply rather than demand. Unlike the second category, the supply chain disruption here is a byproduct rather than the primary goal: the shock doesn’t involve the intentional or targeted weaponization of supply chains, but the disruptions can nonetheless cause meaningful economic damage. This category includes a broad range of shocks with varying degrees of predictability: natural disasters, droughts, factory fires, port congestion, bankruptcies. The collateral supply chain disruptions that might emerge from wars and pandemics can fall into this category as well.

Depending on the specific circumstance, each of the types of contingencies listed above may be a justifiable target of government investment. As a general matter, the highest priority cases for intervention likely fall into the first two categories: responses to public emergencies are classic public goods that demand government investment, and both a growing economics literature and recent experience make clear that firms will not internalize the strategic political costs of supply chain interdependence.

This is not to say all such interventions will be justified, or that no interventions in the third category can be. Ultimately, where taxpayer dollars are best spent will depend on a related but separate inquiry that gets at the value proposition of government investment. Our colleague Todd Fisher has proposed one such framework, which asks whether an industry is compromised (susceptible to the types of contingencies detailed above), critical (directly bearing on US military or intelligence operations, the physical health and safety of Americans, key technologies of future global competition, or foundational industrial inputs), calcified (cannot or will not self-correct), and correctable (susceptible to targeted interventions). Policymakers might also consider the time required to ramp production in a crisis. Where ramp times are short and markets can respond quickly, the case for preemptive government investment weakens; where ramp times are measured in years or decades — as with semiconductor fabs or rare earth processing facilities — the case strengthens considerably.

When it comes to specific industries and goods, the categories may overlap. What made semiconductors such a potent candidate for industrial policy is that they implicated all of the contingencies listed above. The core rationale for the CHIPS Act was geopolitical: with over 90% of leading-edge logic chip production concentrated in Taiwan, the fear of geopolitical coercion drove momentum in Congress during the first Trump administration and early Biden years. But it was the pandemic, and the spectacle of auto factories sitting idle for want of chips, that made the legislation politically potent enough to pass. And because Taiwan is on a large fault line, the risk of an earthquake added a layer of natural disaster concern.

When it came to implementation, the CHIPS team determined that geopolitical coercion posed the biggest risk to US economic and national security, so we ended up concentrating roughly half the portfolio on investments to onshore leading-edge logic chip production and reduce reliance on Taiwan. But we also made investments to strengthen the defense industrial base — category 1 above — that had nothing to do with Taiwan reliance. For example, a modest investment in BAE Systems, which produces critical components for advanced military aircraft and satellite systems out of a facility in New Hampshire, allowed the company to quadruple its production capacity and replace aging equipment, mitigating the risk of operational disruption in the event of a tool breakdown.

What are the sources of resilience?

After determining what contingency they are responding to, the natural next question for policymakers is what it actually means to build resilience. Broadly speaking, there are three potential sources of resilience that can be the target of affirmative industrial strategies.

Stockpiles: Building a stockpile entails producing or procuring a large enough store of goods for future use, either to prevent an external shock from disrupting supply (e.g., China’s efforts to stockpile natural gas, as well as pork, rice, rare-earth metals, and coal, to mitigate the effects of overseas disruptions) or to serve as a short-term buffer during emergency spikes in demand (e.g., the US Strategic National Stockpile of antibiotics, vaccines, and other critical medical supplies meant to supplement state and local supplies during public health emergencies; the Pentagon’s stockpiles of key munitions such as missiles and interceptors; the Strategic Petroleum Reserve, established to reduce the impact of disruptions in supplies of petroleum products). Notably, stockpiles do not have to be public: industrial policy can also incentivize firms to create private inventory reserves. At CHIPS, for example, we sought to build incremental resilience by requiring some of our recipients to maintain certain amounts of inventory as a condition of award.

Existing production capacity: Unlike stockpiling, which involves producing or procuring a set amount of goods before a shock arrives, this category focuses on building ongoing production capacity — e.g., factories, mines, and processing facilities — now so that production is not vulnerable, or is at least less vulnerable, to an external shock. The CHIPS Act is the prototypical example: we invested in building fabs in the United States to help ensure continued access to chips (and the end items that contain chips, from defense systems to data centers to cars to medical devices) in the event of a Taiwan contingency. The presence of internal production capacity doesn’t fully shield a country from external shocks, which can still drive up prices or require shifting production lines to meet domestic demand. But since stockpiles are finite, production capacity is still our most durable source of resilience should a shock occur.

Ramp-up capacity in crisis: A final source of resilience is the ability to ramp up production in a crisis, which could mean both expanding capacity at existing production facilities and/or redirecting manufacturing capacity from other sectors (like how car factories were turned into munitions producers during World War II). Past US forays into industrial policy have involved rapidly scaling up production during war, but the importance of ramp-up capacity extends beyond wartime scenarios. Here, a comparison is instructive: the US was able to quickly increase production of masks during the COVID pandemic, indicating a measure of resilience notwithstanding lack of existing production. But we were unable to quickly ramp production of rare earths when China cut off access in 2025, costing the US major political concessions in US-China trade and technology negotiations.

A few notes on these categories:

These are positive or affirmative sources of resilience, defined by the ability to produce or access physical goods. There are also negative sources of resilience, defined by reducing or eliminating exposure to supply chain vulnerabilities rather than building alternative sources of supply. One such example is China encouraging — and occasionally requiring — domestic industry to replace American inputs with homegrown alternatives.

There have been some American policy efforts that advance negative resilience, such as a congressionally mandated GSA regulation prohibiting executive agencies and government contractors from procuring or using electronics containing semiconductors sourced from China.3 But in our view, the role of negative resilience measures as a part of a broader industrial strategy is an area that deserves considerably more policy thinking.

There are also adaptive responses that governments and firms can deploy, such as investing in new technologies to obviate a current point of vulnerability, cannibalizing old products to reuse parts, and rationing access to lower-value uses of a scarce good to preserve supply for higher-value ones. Particularly in the event of a crisis, policymakers and industry will need to be creative and flexible in fashioning a response.

In any given scenario, the source(s) of resilience that will be most valuable will depend on the particular industry and contingency at stake. Stockpiles will be most valuable where response times are most urgent, such as getting vaccines, PPE, and test kits out during a pandemic. Stockpiles and existing production capacity will help weather or deter geopolitical coercion. And ramp-up capacity will be especially important during a longer war, where attempts at geopolitical coercion will be most aggressive and sustained, and where wartime needs are likely to increase and evolve over time.

The sources of resilience will often be mutually reinforcing: stockpiles can create some demand for existing production, and shoring up existing production capacity is an essential foundation for a successful ramp-up during a crisis. But they require different strategies and should be judged by different metrics of success. For example, a stockpile-based strategy should be assessed based on whether it includes sufficient supply to offset any projected cutoff and/or meet anticipated demand during a crisis. A strategy focused on building existing production capacity should be judged based on whether that production is sufficient to satisfy domestic and allied consumption if an adversary is offline. Both existing production and ramp-up strategies will require sustained investments in an active industrial base, including a trained workforce, functioning educational pipelines, established supplier relationships, operational infrastructure, and increased state capacity around issues like permitting and power and water provision. Ramp-up capacity may also require maintenance of existing production capacity in industries that can be flexibly adapted to other areas (for example, auto manufacturing in World War II).

Importantly, these sources of resilience need not be purely domestic. China currently accounts for roughly 28% of global manufacturing output, a share expected to grow to nearly 40% by the end of the decade. There is no way to compete with that scale of production without what Kurt Campbell and Rush Doshi have called “allied scale” — the United States, Japan, Korea, Europe, and others working together to compete with and provide alternatives to Chinese manufacturing dominance.4 That is doable: the US and its close allies account for the substantial majority of non-Chinese manufacturing output. But it will require real diplomacy, treating allies as true partners in building joint sources of power.

How much resilience is enough?

Once policymakers have determined what contingency they are planning for and what sources of resilience are most needed, the final question is how much resilience is enough. As Jake Sullivan recently put it, “complete, permanent resilience in all critical goods is likely out of reach.” It would be prohibitively expensive — and therefore poor government policy — to onshore, or even friend-shore, every critical dependency, or to anticipate every possible external shock. But if full resilience is impossible, can partial resilience still justify industrial policy?

In the context of pandemic preparedness and large-scale military conflict, the answer is a relatively straightforward “yes.” It is not possible to identify and prepare for every conceivable emergency shock; policymakers should instead identify the most likely and/or damaging contingencies and work backward to determine what level of production, stockpiling, or ramp-up capacity is required. And in the context of a particular emergency, an investment in partial resilience — for example, stockpiling vaccines but not masks — is still likely to be valuable on the theory that something is better than nothing.

The question is more complicated when it comes to geopolitical coercion, where there is a less straightforward return on investment: if partial resilience does not actually meaningfully reduce an adversary’s leverage, then it will have been a waste of taxpayer money. Determining whether partial resilience is worth the investment requires distinguishing between two kinds of resilience: resilience across industries (horizontal resilience) and resilience within a single industry (vertical resilience). As detailed below, partial horizontal resilience is likely worth it; partial vertical resilience less so.

Horizontal resilience

Partial horizontal resilience means building resilience in some critical industries (e.g., semiconductors) while remaining dependent on an adversary — here, we focus specifically on China — for others (e.g., active pharmaceutical ingredients). Ideally, the US would reduce dependence on critical Chinese chokepoints wherever possible. But even partial resilience across industries is likely to reduce China’s overall economic leverage and increase US bargaining power by lowering the costs it would face in a US-China conflict.

The relationship between chokepoints and leverage is likely non-linear because leverage depends on an adversary’s ability to activate or threaten to activate multiple pressure points simultaneously. An adversary with one chokepoint may hesitate to cut off access for fear that its opponent will weather the harm, make investments to neutralize the chokepoint, and/or retaliate economically elsewhere; an adversary with multiple chokepoints can more realistically engineer or threaten to engineer a crisis that will be much more costly to withstand. Reducing chokepoints across industries could therefore yield substantial returns, reducing the overall power of an adversary’s coercive arsenal.

Of course, a country with even one chokepoint can wield coercive leverage in a crisis if weaponizing that chokepoint would be sufficiently catastrophic for its adversary; more theoretical and empirical work is needed to understand just how much — and under what conditions — partial horizontal resilience reduces an adversary’s strategic power. Broadly speaking, though, we should not let the impossibility of addressing all dependencies deter us from addressing the most critical ones. The CHIPS Act itself was a recognition that addressing one critical chokepoint is better than doing nothing.

When deciding which industries to tackle first, Washington should have some theory of how China can or intends to weaponize chokepoints during a crisis, and how this would affect the US economy and national security. This will allow us to prioritize the industries where China is both most willing to act and where lack of access would be most damaging.

Vertical resilience

Partial vertical resilience is a different story. Consider a hypothetical industry that has three primary nodes in its supply chain: the manufacturing of the good itself, the inputs needed to manufacture the good, and the downstream finishing of the product. Now suppose Congress passes a bill to onshore manufacturing of the good but provides no funding to onshore the upstream inputs or downstream finishing. If China controls production of either the inputs or the finishing — or both — then the bill may not succeed in reducing China’s leverage. By cutting off other nodes in the supply chain, China can render the US onshoring effort impotent: the country will have reduced dependence on China for the manufactured good while remaining dependent on China for the input required to make and finish it, at considerable expense and no reduction in exposure.

At CHIPS, this logic drove us to prioritize onshoring not just chip manufacturing but also capacity for advanced packaging, one of the final stages of chip production. Like chip fabrication, advanced packaging for logic chips is concentrated in Taiwan, which has nearly all of the most advanced global capacity; in a Taiwan contingency, China could disrupt US access, leaving the United States with nearly finished chips but few options to complete production. Before CHIPS, the US share of global advanced packaging capacity was close to zero. We made securing advanced packaging a top programmatic priority and had considerable success in advancing that goal: Intel, Amkor, TSMC, and SK Hynix are now all undertaking advanced packaging projects in the United States. In some cases, we also included terms in our deals with chipmakers requiring them to package their chips outside of China and Taiwan.5

The lesson here is that within a supply chain, a single missing part can halt production entirely. Unlike resilience across industries, resolving nine of ten chokepoints within an industry may get you little if the tenth is a single point of failure. Of course, the value of partial vertical resilience will depend on the extent to which the missing chokepoint is a true point of failure; one could imagine a strategy of partial vertical resilience making sense where that missing chokepoint would be relatively easy or cheap to ramp up during a crisis. In general, though, policymakers designing and implementing industrial policy within an industry should seek to understand its entire supply chain with an eye toward addressing all known areas of vulnerability, while of course relying on allied production capacity to fill any gaps.

How much supply is enough?

Notably, however, the imperative for vertical resilience does not require industrial policy to secure fully resilient supply for all domestic demand. Economists Clayton, Maggiori, and Schreger conclude that “power is nonlinear and increases disproportionately as the hegemon approaches controlling the entire supply of a sectoral input.” The reverse implies that as a hegemon’s control falls away from total, its leverage degrades faster than the market share numbers suggest. This means that achieving, say, a quarter of domestic production of a critical input can yield much more than a quarter of the strategic benefit. In Clayton, Maggiori, and Schreger’s words, even modest diversification can result in “much economic security… with little overall fragmentation.”

As a result of the CHIPS Act, the US is expected to increase its share of leading-edge logic production from nearly zero to between one-fifth and one-third. A skeptic might note the meaningful dependence that remains. But when one considers various Taiwan scenarios, having a thriving domestic industrial base for leading-edge logic chips — one of only one or two in the world outside of Taiwan — will be of immense strategic value. Consistent with the Maggiori finding, that value is likely to exceed what the market share numbers alone would suggest.

Further investigation

The questions we’ve set out here — what is resilience and what do we need it for, what are the sources of resilience, and how much resilience is enough — have concrete, real-world implications for industrial policy. The first tells policymakers when government intervention may be warranted and can help them decide which industries to prioritize; the second informs the focus of that policy and the metrics by which its success should be judged; and the third can help policymakers make optimal portfolio allocations or design an omnibus industrial policy bill.

We hope others will continue where we’ve left off, researching and proposing answers to questions such as:

How, concretely, should success be measured across the three sources of resilience (stockpiles, existing production capacity, ramp-up capacity in crisis)? Do these measures change depending on the contingency?

What might a robust theory of friendshoring look like in an era of fractured alliances and an increasing desire for technological and industrial autonomy among middle powers worldwide?

How can we quantify the strategic value, or lack thereof, of horizontal and vertical resilience?

In the context of building resilience to Chinese coercion, if full horizontal resilience is not feasible, how should we prioritize the next phase of industrial investment?

Just as practice needs theory, theory needs practice: ultimately, we hope the answers to these questions will galvanize policymakers to consider what the next CHIPS should be — what industry or industries to target, to what end, and on what scale. This exercise should not remain purely analytical. There is broad bipartisan consensus on the importance of resilience as a strategic objective, a rare area of agreement in an otherwise fractured political landscape. What has been missing is a sustained effort to channel that consensus toward a comprehensive national industrial strategy that identifies priority industries across the full range of critical supply chains and empowers the government to address them. The CHIPS Act was a beginning; the analytical framework we have sketched here draws on that experience to lay the groundwork for what might come next.

15 U.S. Code § 4652, which codified the CHIPS incentives program, included multiple references to “resilience” or “resiliency,” including a requirement that the Secretary “give priority to covered entities that support the resiliency of semiconductor supply chains for critical manufacturing industries in the United States.”

This post discusses industrial policy focused on the production of and access to physical goods. It does not cover other policy areas, such as investments in innovation and R&D, that may have overlapping and distinct rationales.

The GSA regulation also had policy objectives beyond supply chain resilience, most prominently reducing the risk that adversaries could infiltrate sensitive government supply chains, e.g., through introducing “hardware, backdoors, malicious firmware, and malicious software into a semiconductor.” How best to protect against national security risks from technology imported from other countries is a separate policy question that also deserves more thinking.

A non-manufacturing analogue: the International Energy Agency petroleum stockpiles — through which 32 members hold emergency stockpiles of over 1.2 billion barrels — were established in 1974 in response to the OPEC embargo to counter vulnerability to oil from Arab producers.

We did not treat all foreign chokepoints alike. Like advanced packaging, Extreme Ultraviolet Lithography (EUV) is an essential part of the leading-edge semiconductor supply chain, and Dutch firm ASML produces every EUV machine in the world out of its facilities in the Netherlands. We considered whether to make a major push for EUV manufacturing in the United States but concluded that the geopolitical case did not warrant it: unlike Taiwan, the Netherlands is a close NATO ally whose concentration of EUV production represents a supply chain dependency, but not a vulnerability of the kind that animates our concern about Chinese chokepoints. Our limited resources were better deployed addressing dependencies that a strategic adversary might actually exploit.